- News

- Business News

- India Business News

- HC sets aside CBDT’s plan of rewarding CITs-appeal

Trending

This story is from April 23, 2019

HC sets aside CBDT’s plan of rewarding CITs-appeal

As the financial year 2018-19 was coming to a close, CBDT apprised the court that it would carry out the requisite amendments in the action plan for the next financial year 2019-20.

")

(Representative image)

Key Highlights

- CBDT’s action plan for the financial year 2018-19 had set out that the CITs-A would be allowed additional performance credits of two units for every quality appellate order passed.

- The term ‘quality’ orders included cases where the CIT-A enhances the order of the I-T officer (in other words, the quantum of tax demand is increased) or where he strengthens the order of the I-T officer

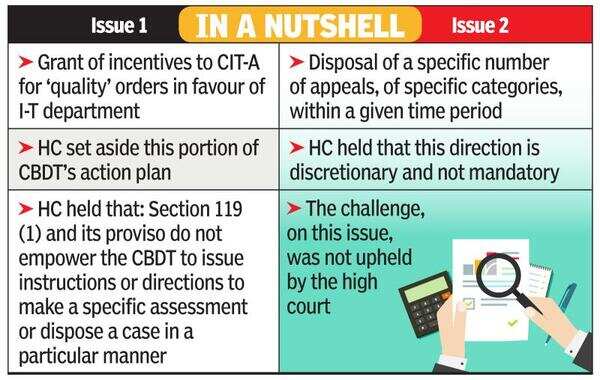

MUMBAI: The Bombay high court has set aside that portion of CBDT’s action plan that sought to incentivise commissioners of income tax-appeals (CITs-A) who pass ‘quality’ orders, which could be detrimental to taxpayers.

“Any temptation in the guidelines, referred to as incentives for disposal of an appeal in a particular manner would not stand the test of law,” the high court held in its written order made available on April 22.TOI, in its edition dated March 27, had reported on the interim order where the high court had asked the Central Board of Direct Taxes (CBDT) to reconsider this aspect and apprise it on the steps that would be taken.

As the financial year 2018-19 was coming to a close, CBDT apprised the court that it would carry out the requisite amendments in the action plan for the next financial year 2019-20.

CBDT’s action plan for the financial year 2018-19 had set out that the CITs-A would be allowed additional performance credits of two units for every quality appellate order passed. The term ‘quality’ orders included cases where the CIT-A enhances the order of the I-T officer (in other words, the quantum of tax demand is increased) or where he strengthens the order of the I-T officer. It also included instances where the CIT-A levies a penalty on the additions confirmed by him to a taxpayer’s income.

When taxpayers dispute their tax demands, raised by the I-T officer, they approach the CIT-A. This is the first level of appeal. Based on facts of the case and legalities involved, orders passed by the appellate commissioner can swing either in favour of the taxpayer or the I-T department.

Tax experts had pointed out that CBDT’s action plan may prejudice the minds of the CITs-A. This led to The Chamber of Tax Consultants, a not-for-profit body of tax professionals, filing a petition in the high court. Speaking to TOI, Hinesh R Doshi, president of the Chamber of Tax Consultants, termed the verdict as a major victory for taxpayers.

He also referred to CBDT’s future plan of action. For the financial year 2019-20, the board would modify the definition of quality orders to include all appeal orders passed by the CIT (A), whether decided in favour or against the revenue, where the supervisory commissioner is of the view that the CIT(A) has devoted more time. This would refer to the time spent for ascertaining the facts and passing exceptionally well-reasoned order, which takes into consideration applicable judicial precedents. “Thus, the grounds for bias would be eliminated,” Doshi said.

The high court noted that while the CBDT has wide powers under section 119(1) to issue orders, instructions and directions to other I-T authorities, as it may deem fit, for proper administration of the I-T Act, it does not empower the CBDT to issue instructions or directions to make a particular assessment or dispose a case in a particular manner. It also observed that appellate commissioners have already passed orders under the shadow of the incentivisation programme contained in the action plan. In this background, tax experts point out that this order of the high court gives a better standing to aggrieved taxpayers, when they appeal against orders of the appellate commissioners.

The Chamber of Tax Consultants had also challenged the directions issued by the CBDT in its action plan for disposal of a certain number of appeals of specified categories, within a specified period of time. The high court did not find this direction as objectionable.

“Any temptation in the guidelines, referred to as incentives for disposal of an appeal in a particular manner would not stand the test of law,” the high court held in its written order made available on April 22.TOI, in its edition dated March 27, had reported on the interim order where the high court had asked the Central Board of Direct Taxes (CBDT) to reconsider this aspect and apprise it on the steps that would be taken.

As the financial year 2018-19 was coming to a close, CBDT apprised the court that it would carry out the requisite amendments in the action plan for the next financial year 2019-20.

However, coming down strongly against the plan to incentivise appellate commissioners for quality orders, the court held: “...the guidelines in its existing form for the past financial year also cannot be allowed to have effect.”

CBDT’s action plan for the financial year 2018-19 had set out that the CITs-A would be allowed additional performance credits of two units for every quality appellate order passed. The term ‘quality’ orders included cases where the CIT-A enhances the order of the I-T officer (in other words, the quantum of tax demand is increased) or where he strengthens the order of the I-T officer. It also included instances where the CIT-A levies a penalty on the additions confirmed by him to a taxpayer’s income.

When taxpayers dispute their tax demands, raised by the I-T officer, they approach the CIT-A. This is the first level of appeal. Based on facts of the case and legalities involved, orders passed by the appellate commissioner can swing either in favour of the taxpayer or the I-T department.

Tax experts had pointed out that CBDT’s action plan may prejudice the minds of the CITs-A. This led to The Chamber of Tax Consultants, a not-for-profit body of tax professionals, filing a petition in the high court. Speaking to TOI, Hinesh R Doshi, president of the Chamber of Tax Consultants, termed the verdict as a major victory for taxpayers.

He also referred to CBDT’s future plan of action. For the financial year 2019-20, the board would modify the definition of quality orders to include all appeal orders passed by the CIT (A), whether decided in favour or against the revenue, where the supervisory commissioner is of the view that the CIT(A) has devoted more time. This would refer to the time spent for ascertaining the facts and passing exceptionally well-reasoned order, which takes into consideration applicable judicial precedents. “Thus, the grounds for bias would be eliminated,” Doshi said.

The high court noted that while the CBDT has wide powers under section 119(1) to issue orders, instructions and directions to other I-T authorities, as it may deem fit, for proper administration of the I-T Act, it does not empower the CBDT to issue instructions or directions to make a particular assessment or dispose a case in a particular manner. It also observed that appellate commissioners have already passed orders under the shadow of the incentivisation programme contained in the action plan. In this background, tax experts point out that this order of the high court gives a better standing to aggrieved taxpayers, when they appeal against orders of the appellate commissioners.

The Chamber of Tax Consultants had also challenged the directions issued by the CBDT in its action plan for disposal of a certain number of appeals of specified categories, within a specified period of time. The high court did not find this direction as objectionable.

About the Author

Lubna KablyEnd of Article

FOLLOW US ON SOCIAL MEDIA

Hot Picks

TOP TRENDING

Trending Stories

In Business

Entire Website

- Will banks open only for 5 days a week? Here’s what you should know about IBA’s proposal

- India set to be third largest economy, says S&P Global

- Dalal Street bull run continues! BSE Sensex crosses 69,000 for the first time; Nifty above 20,800

- Byju’s reduces notice period for employees as troubles mount

- Sensex surges over 900 points, Nifty above 20,550 as BJP state election wins bolster Modi's Lok Sabha 2024 prospects

- UltraTech to buy building materials business of Kesoram in 7,600 crore deal

- Tata Technologies stock debuts at a bumper 140% premium; share price at Rs 1200 on BSE

- Tata Technologies share allotment: How to check IPO allotment status, listing date, GMP

- BSE m-cap rides rally in Adani stocks, tops $4 trillion

- Charlie Munger, who helped Warren Buffett build Berkshire, dies at 99

- In Madhya Pradesh, Congress struggles to break saffron stranglehold on 6 seats

- Akhilesh to contest from Kannauj seat, to file nomination tomorrow

- Will welfare schemes help Cong spring a surprise in Karnataka?

- 'PM trying to mislead people with lies': Priyanka

- Shubman Gill joins Sehwag and Gambhir in this elite list

- Cong into damage control mode amid backlash over Pitroda's comments

- Six ways to fix range anxiety faced by EV owners in India

- Infosys 1st co to achieve this certification in AI management: CEO

- IPL Live: Delhi Capitals lose Fraser-McGurk after solid start

- 'All 3 units of EVMs have their own microcontroller'

Popular Categories

Hot on the Web

Top Trends

DC vs GT Live ScoreTS Inter ResultsTelangana Inter ResultsMP Board 10th Result 2024MP Board Result TimeIPL Today MatchWorld Fastest Cruise MissileCUET UG Date SheetNEET UGKotak Mahindra BankIPL Orange Cap 2024IPL Purple Cap 2024IPL 2024 ScheduleLok Sabha Election Full ScheduleIPL Points TableIPL Match Full Schedule

Trending Topics

Arti SinghEverest MasalaOptical IllusionKiara AdvaniMonthly Health HoroscopeRajkumar RaoPink Full Moon 2024Monthly Career HoroscopeRavi KishanPink MoonMunawar FaruquShilpa ShettyAmitabh BachchanChiranjeeviRupali GanulyParineeti ChopraBest Ceiling LightsBest Whey ProteinBest Office Handbags For WomenBest 24 Inch Tv

Living and entertainment

Latest News

Independent travel high on Gen Z's mind: Skyscanner surveyInspired by ‘Krishna Mohini’, ‘Dance Deewane’ judge Suniel Shetty credits his kids Ahaan and Athiya as his saaRthiShubman Gill joins Virender Sehwag and Gautam Gambhir in this elite listWhy Congress looks poised to win battle of INDIA allies in KeralaCongress says BJP's conspiracy to create political crisis in Himachal failed; BJP retaliates by calling congress 'flop government'Congress says BJP's conspiracy to create political crisis in Himachal failed; BJP retaliates by calling congress 'flop government'Congress says BJP's conspiracy to create political crisis in Himachal failed; BJP retaliates by calling congress 'flop government'This company may beat Microsoft, Google, Amazon and others to become Nvidia's biggest AI chip customerWatch: Sayli Salunkhe answers fan questionsRafael Nadal will only play French Open if he can 'compete well'Shekhar Suman says that everyone lied about Parveen Babi that she was mad, though he cut out many portions from his interview with herDiatoms will never let this man’s name dieConductor falls off Trichy city bus along with seatConductor falls off Trichy city bus along with seatFormer UP CM Akhilesh Yadav to contest from Kannauj seat, to file nomination tomorrowLok Sabha elections: Lost Your Voter ID? Here's how to get a replacementLok Sabha elections: Lost Your Voter ID? Here's how to get a replacementLok Sabha Elections 2024 Phase 2 in MP: Schools and colleges to remain shut in these constituencies

Copyright © 2024 Bennett, Coleman & Co. Ltd. All rights reserved. For reprint rights: Times Syndication Service